Project Summary

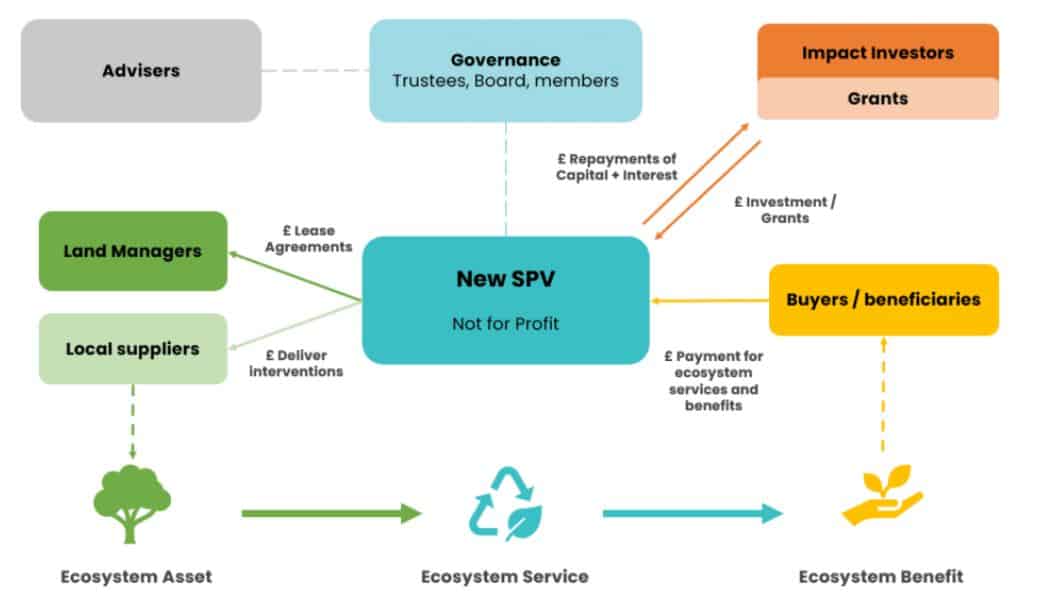

The Wyre Catchment Natural Flood Management Project is the first example in the UK of the use of repayable private investment enabling the delivery of natural flood management. The project will deliver more than 1,000 targeted measures to store, slow and intercept flood water and prevent peak flow in a catchment in England, with the interventions hosted by local farmers. Beneficiaries of the reduced flood risk are paying for the interventions through an extendable nine-year contract, and the Project’s Community Interest Company has successfully raised a nine-year £850k private loan facility to help fund the up-front capital cost of the interventions.

Acknowledgements

With many thanks for their time and insight on this case study:

Dan Turner, Technical Lead, Land Management and Market Creation, The Rivers Trust

Dan Hird, Principle and Founder, Nature Finance

Nominating key decision makers

Now operational, the project is governed by a board of seven voluntary directors who represent the key stakeholder organisations in the project and Wyre catchment.

In developing this governance structure, the project team recognised that many stakeholders who were involved in the development of the project would have an interest in remaining involved once operational. The project team also wanted to retain the collaborative and ‘open book’ approach it had taken throughout project development, so it decided that a board of voluntary directors with a flat hierarchy would be most appropriate.

In order to ensure this, the Articles of the CIC make provision for the following stakeholder representatives as directors on the board

- The Wyre Rivers Trust

- The Rivers Trust

- The buyers

- The land managers

- The investors

- The local community

- An independent chair

Each director representative is responsible for reporting on the project’s performance back to their respective stakeholder groups and taking feedback, requests and questions to the board. Individuals to represent these groups were chosen for different reasons.

For example, the Wyre Rivers Trust and Rivers Trust nominated their Chairman and Chief Executive Officer respectively. The Trusts are responsible for providing key services to the project under contractual agreements and it was agreed that these senior members could sufficiently represent the Trusts while managing any conflicts of interest associated with the provision of these services. The Wyre Rivers Trust is responsible for the installation and monitoring of the interventions and continued engagement through a Project Delivery and Management Services contract. The Rivers Trust is responsible for the finance, administration and company secretarial aspects of running the Community Interest Company through an Asset Management Contract.

The buyer group and land manager group have each nominated a representative on the understanding that the individual representative is likely to rotate every two years. This rotation was agreed so that members of these more diverse groups are fairly represented over the lifetime of the project, and no one individual or individual organisation is becoming overburdened or ‘entrenched’ in their director position.

During investor negotiations it became clear that the group of 5 impact fund investors were keen to see director representation on the CIC board although this was not specifically requested by the four high-net-worth individuals (see Milestone 7). As Dan Hird who was Head of Corporate Finance at Triodos Bank had personally led on the investment readiness and capital raising activity, their was mutually agreed between the project team, the investors and Hird, that he should stay on as the investor representative on the board for at least the first 12 months to ensure some continuity. This was also a benefit to the project as Triodos Bank’s role as advisor came to an end on completion of the transaction, but Hird’s remaining presence as a director would help retain the commercial expertise that Triodos had provided.

The project team was keen to include a community representative from Churchtown on the board, in order to align one of the project’s target outcomes (flood risk reduction and resilience to local residents) with its governance structure. A member of the local flood action group, who had been active in engaging with the project during development (see Community Engagement) was chosen, though likewise this position will see a periodic rotation between nominated community members.

Finally, it was decided that the project needed an independent director to serve as Chair with no commercial or other major interests in the project, in order to provide an impartial view and help resolve any disagreements on the board. Gary Hueting, COO of Markerstudy, was nominated and agreed to accept the role. Gary was previously COO of Co-op Insurance (before it was acquired by Markerstudy in 2020) and he was personally engaged in the project’s early development. The project team felt that Gary would make an excellent chair, given his prior knowledge of the project, strong commercial skills and experience and personal interest in better engaging the insurance sector in natural flood management.

The CIC board meets once every three months and every member has an equal voting right in decisions, requiring two thirds of the director to agree for a decision to be approved. The quorum, conflicts resolution strategy and director nomination processes are also set out in the company’s Articles, as part of the project’s governance structure and legal incorporation (see below).

Performance reporting

To inform decision making, the CIC board receives two standing quarterly updates from Wyre Rivers Trust and The Rivers Trust. These updates are a reporting requirement in the Project Delivery and Management Services Contract and the Asset Management Contract respectively.

The initial main focus of the Project Delivery and Management Services Contract from Wyre Rivers Trust is the progress of the installation of the NFM interventions over the first four years. This is to make sure that the project is on track to deliver, including on its contractual agreement with buyers that 80% of the NFM interventions must be installed in the ground by the end of the third year.

As these interventions are installed, the project will also begin to accumulate performance data, namely how effective these interventions are at reducing peak flow during a one-in-50 year flood event. Measurement of the performance data will be undertaken post-weather events by the Wyre Rivers Trust, which will use various equipment, including flumes, level loggers and timelapse photography. The Wyre Rivers Trust will also conduct site visits annually to check that the interventions are being maintained and working well otherwise.

This data will be shared with the board members and will be key for the adaptive management phase of the project, which is a five-year phase that allows the interventions to be optimised before buyer payments move from being installation based to performance based (See Milestone 3). The project team agreed this data will also be important to build an evidence base for natural flood management projects in other areas.

Board reports are provided by email ahead of board meetings. However, in the future the project team also plans to develop an ‘NFM Dashboard’ that uploads all performance reporting of the project to a website that can be updated regularly and viewed on demand by key stakeholders including not only the board, which will have full view of the performance data, but also the general public, who will have a public view mode that will be used to engage and inform external stakeholders with high interest, such as community volunteer groups, local businesses, Catchment Based Approach (CaBA) partnerships.

In addition to this public NFM dashboard view, the project also plans to publish a full evaluation report of the project at the end of the initial nine years, which will give a comprehensive assessment of the project’s delivery, effectiveness in reducing flood risk and other important outcomes.

Choice of legal entity

Following advice from Triodos and a thorough review of alternative structures, a Community Interest Company (CIC) limited by guarantee was selected as the optimum special purpose vehicle for the project. The Wyre Catchment CIC was officially incorporated in June 2021 and the project formally completed on 31 March 2022.

When considering the types of legal entity to use, the project team conducted a Red Amber Green (RAG) assessment of most types of entities, such as Community Benefit Societies, Companies Limited By Shares and Co-operatives.

As part of the evaluation process, the project team considered a number of factors including: engagement of multiple stakeholders, need for external repayable private investment, risk profile etc. Because of the project’s core mission and the fact the an environmental charity (the Rivers Trust) would be running the legal entity, the project team felt strongly that neutral ownership would be an advantage, and that the choice of legal entity should reflect the fact that this project exists primarily to benefit the local community.

As a result, a CIC limited by guarantee was chosen with a 100% asset lock in the Articles – ensuring any profits or other assets withdrawn from the profit would only be used for projects of benefit to the local community. The project team considered this entity type to sit halfway between a private company and a charity, structured as a social enterprise but with a similar level of flexibility as a private company. Once the decision was taken, it only took half a day to actually set up the company and register it at Companies House and with the CIC Regulator. A CIC is also capable of taking on private investment, but in this case, this would only be debt-based investment due to the fact that it does not have share capital.

The project team submitted its CIC application to Companies House for £27, along with its ‘community interest statement’, explaining what the project plans to do to benefit its community. This application was assessed by the CIC Regulator, a department within Companies House. As part of ongoing reporting requirements, the project team must file an annual community interest report that is placed on the public record at Companies House and copied to the CIC Regulator. The report must include details of the remuneration of the directors and interest paid on the loans. It will also need to explain what the CIC has done to benefit the community and how it has involved community members in its activities. This report will be drawn together by the board and submitted by the director representing the Rivers Trust, as part of their administrative and management responsibilities.

After announcing its intention to form a CIC, the project team noted a positive reception from its partners and external stakeholders, such as the land managers, community groups, and investors. The project team believes that the community focus embedded within this entity type made the team’s stated ambition more credible and helped with remaining engagement, such as signing land managers onto the project.

However, one small drawback was the fact that the CIC was newly formed and therefore did not have a financial history. This made administrative dealings with larger project partners, such as the Woodland Trust, slightly more difficult as these organisations had procurement and risk policies that viewed companies with limited financial history as more risky. This made some ‘workaround’ solutions necessary. For example, the Woodland Trust ultimately agreed to enter into a tree planting grant agreement with the Wyre Rivers Trust directly, instead of through the CIC – albeit the terms of this agreement were negotiated by the CIC and project team.

The Rivers Trust also note that, with the longer-term ambition of replicating the project’s blueprint in other catchments with flood risk, it will need to find a way to ‘nest’ any further CICs within a common structure, to make sure these are managed correctly and the Rivers Trust are delivering on its obligations.

Lessons Learned

Hird comments that there were many lessons learned from the governance development phase, and has set out the below points for other project developers to note:

- Consider what your intermediary vehicle is going to be, because most projects will need some sort of Special Purpose Vehicle (SPV) to contract with the various parties, handle money flows and then offer governance post completion. This decision stage does not need to involve lawyers or significant cost, as the project team should be in a position to independently consider the pros and cons of each legal entity type, with a wealth of information on this available online.

- Once you’ve decided what the form of your SPV is going to be, you can communicate this to various stakeholders and partners, which will give them more certainty, but suggest you don’t necessarily need to set this up yet (so again no legal costs) until you know you have achieved an investable transaction.

- When there comes a point in the project where you are confident you are going to “get there” or feel you just need to have the vehicle established for some reason (see below) then you could either set it up yourself or ask a legal firm to set it up.

- Reasons why you might want to set the SPV up prior to completion include:

-

- Needing to have an actual company or vehicle on the front of your MoUs for credibility purposes if you are negotiating with large organisations,

- Because you want to set up a bank account in advance of completion, which can take months,

- You want to register for VAT or HMRC or SITR Clearance – and HMRC will want to know which organization is applying.

- When you do set up your SPV, think carefully about how many directors you want to appoint on Day One. For example, if you appoint seven directors, this will take a lot of administration time with forms, and any bank will want to do diligence on all directors before setting up an account. Formal project decisions on daily issues could also become unwieldy with multiple registered directors. Instead, consider appointing the minimum two directors only (as with the Wyre Rivers NFM Project), which means you only need two people to approve decisions in the project development phase. This is much more agile in a complex transaction. Other directors can then be appointed at or immediately after completion.

- Regarding time efficiency and project governance, it is important to think carefully about project management and there is a danger of too much project governance – steering groups, project boards, meetings etc could all suck time from the core project team who will have a lot to do on a small budget. As a preferred example, consider operating as a project team that works together daily and a Project Steering Group that meets quarterly.