Policy and Regulation

Project developers and enterprises will need to keep a continuous check on how current and future policy may affect the project, and also opportunities for the project to inform policy. The role of private finance for nature across the UK is being encouraged by the UK government and its devolved administrations, and new rules, standards and markets are being developed.

Policy and Regulation has been divided here into two themes for consideration. Click on each of these themes to the right to read more.

UK Nature-based Standards and Codes

Across the UK, many codes and standards are emerging that will allow for the sale of credits from nature restoration. These codes focus on different natural habitats and are led by separate groups, such as Wildlife Trusts, research institutes and other non-governmental organizations.

You can find a useful overview of the current codes and standards

Below is a summary of the nature-based codes and standards in the UK, including those that are operational and under development. These focus on carbon, but will be expanded to include other types of codes as they come into development.

Note: there are other codes in early development, such as the Seagrass Carbon Code, the Sussex Bay Kelp Carbon Code and the UK Freshwater Biodiversity Code. These do not yet have their scientific grounding laid out, and some may be incorporated into other emerging codes.

Code |

Brief overview |

Launch Date |

Other information |

| Woodland Carbon Code

|

Supports the creation of new woodlands in the UK. Multiple woodland types are eligible, including native woodlands with minimum intervention, to commercial woodlands under regular clear-felling.

As of 31 December 2022, there are over 1,800 projects registered under the Woodland Code that cover 67,000 hectares. This includes 1,400 projects that are under development and 425 projects that are validated and expected to sequester 8 million tons of carbon over their woodland’s lifetime. You can view these statistics in more detail here. |

2011 | Woodland Carbon Code units are being purchased at around £20-£40 per unit.

Verified Woodland Carbon Units (WCUs) are based on existing carbon being taken out of the atmosphere, and so are permitted under the SBTi’s ‘Net Zero’ carbon accounting framework. Pending Issuance Units (PIUs) effectively a ‘promise to deliver’ a Woodland Carbon Unit in future, based on predicted sequestration. It is not ‘guaranteed’, and cannot be used to report against UK-based emissions until verified. However, it allows companies to plan to compensate for future UK-based emissions, or make credible CSR statements in support of woodland creation The UK Government offers project developers the Woodland Carbon Guarantee, which provides the option to sell their verified units (WCUs) for a guaranteed price every 5-10 years up to 2055/56.

|

| Peatland Code

|

Supports the restoration of degraded bog peatlands in the UK, which currently emit more carbon every year than UK woodlands sequester.

As of 8th of March 2023, there are 157 projects registered under the Peatland Code, including 130 projects under development and 27 validated projects which are collectively expected to avoid 900,000 tons of carbon emissions over the lifetime of their restored peatlands. You can view these statistics in more detail here. |

2015 | Units under the Peatland Code are currently being purchased between £15-£30 per unit.

Verified Peatland Carbon Units (PCUs) are based on avoiding further emissions and are therefore not permitted under SBTi’s ‘Net Zero’ carbon accounting framework. They are however permitted under the definition of ‘Carbon Neutral’, as set out by PAS2060. As with the Woodland Carbon Code, it also allows the sale of PIUs. In March 2023, the Peatland Code released its Version 2.0 that includes ‘fens’ peatlands, which have often been converted to crop fields. It is expected that projects that focus on restored fens will deliver much higher volumes of carbon emission reductions, and therefore more units for sale.

|

| Wilder Carbon Standard

|

Supports native habitat restoration in the UK to target both carbon and biodiversity benefits. Aims to restore landscapes that host multiple habitats using one assurance mechanism.

The Wilder Carbon Standard is governed by a panel of independent cross-sector experts, including several Wildlife Trusts. The Technical Standard Board who act as guardians of the standard are further developing it and assuring it is applied in practice. It currently has two live projects with conservation-grade carbon units, validated by the Soil Association Certification and available to purchase upfront as Estimated Issuance Units (EIUS). The indicative project pipeline is estimated to facilitate a megaton of carbon lock up each year to 2030.

|

2021

Version 2 to be published in early 2023 |

Eligible habitats include natural regeneration of woodland, arable reversion to grassland and wood pasture, rewetting of coastal saltmarsh or riverine floodplains, and rewetting of drained peatlands.

It also facilitates Research and Development projects where good carbon data doesn’t currently exist for the sale of units post verification. The Standard includes an Approved Buyer criteria that only permits sales of Wilder Carbon credits to UK registered companies that have a public commitment to Net Zero with a credible delivery plan, among other requirements. This project is being supported by the Natural Environment Investment Readiness Fund, which gave funding to the project in its first round in 2021.

|

| Minimum Requirements for Soil Carbon Projects

(formerly the Soil and Farm Carbon Code)

|

A set of minimum standards, against which existing codes and projects are evaluated in order to function in the UK marketplace.

Aims to support the needs of UK soil carbon projects that are not viable or served by existing carbon codes. The Minimum Requirements will address the following three elements of each soil carbon code and project:

The Minimum Requirements have been developed by a consortium of leading soil scientists and international carbon protocol experts. The Sustainable Soils Alliance have led stakeholder engagement and project co-ordination. In December 2022, the project team published its Recommendations on minimum requirements for high-integrity soil carbon markets in the UK.

|

Estimated 2023+ | UK soils store over 10 billion tonnes of carbon in the form of organic matter. Roughly equal to 80 years of annual UK greenhouse gas emissions. However, it is estimated that in the UK, soil is being destroyed 10 times faster than it is being created.

The project team is also developing a Route Map to an open access, community code that will be aligned with the minimum requirements that can be used by new entrants and small-scale projects that are not served by the existing codes and/or marketplace because of technical challenges or high up-front cost. To support this wider work, the project team undertook a review of existing soil carbon codes internationally, including what makes them operational. This project is being supported by the Natural Environment Investment Readiness Fund, which gave funding to the project in its first round in 2021.Project funding was obtained by FWAG South West . |

| Hedgerow Carbon Code | Aims to support the creation of new hedgerows and improvement of existing hedgerows across the UK.

The Code is being developed at its demonstration farm, the Allerton Project, led by the Game and Wildlife Conservation Trust. The project team is now using a trial Hedgerow Carbon Code across three arable farms in England. It includes a tool that will enable the carbon stored in a hedge to be calculated as a means of incentivising farmers to make further improvements. The tool also has the potential to be developed further to monitor hedgerow biodiversity for calculating biodiversity credits. |

Estimated 2023+ | Early research shows hedgerows sequester carbon at twice the rate of woodlands (per hectare) due to their three dimensional structure.

There are 402,000 km of hedgerows in Britain that are in good condition, a further 145,000 km that are in poor condition, and a further 26,000 km that can no longer be classified as hedgerows due to degradation. It is estimated that British hedgerows currently store around 9m tonnes of carbon, valued at £65m at base carbon prices (£7 per tonne). The project team estimates that there is enormous potential to increase by improving and expanding hedgerows, potentially delivering up to £60m additional income to farmers and other land owners. This project is being supported by the Natural Environment Investment Readiness Fund, which gave funding to the project in its first round in 2021.

|

| Agroforestry Carbon Code | Aims to support agroforestry practices in the UK – where trees are deliberately combined with agriculture on the same piece of land. This covers certain practices supported by the Woodland Carbon Code and possibly the Hedgerow Carbon Code, as well as unique carbon measurement protocols for in-field trees in silvoarable and silvopasture systems.

This project is coordinated by the Soil Association, in partnership with Woodland Trust, Organic Research Centre, Finance Earth, Scottish Forestry and Scotland’s Rural College. The project team is running pilots on five sites to understand lifetime costs for agroforestry systems and other data.

|

Estimated July 2023+ (for completed feasibility) | It is estimated that only 3.3% of the area used for agriculture is managed as agroforestry currently in the UK, however this type of farming is considered to have huge potential to combine the benefits of trees with a productive farming landscape.

This project is being supported by the Natural Environment Investment Readiness Fund, which gave funding to the project in its second round in 2022. |

| UK Saltmarsh Carbon Code | Aims to support the restoration of degraded saltmarshes, covering up to 22,000 hectares in the UK.

The Code development is being led by the UK Centre for Ecology and Hydrology (UK CEH), supported by Finance Earth. Principles to develop a UK domestic code will be prepared by December 2022. Research undertaken by the team shows that newly restored marshes have sequestration rates of carbon between 13 – 15 tonnes of CO2e per hectare per year, compared to around 5.9 – 8.2 tonnes in natural marshes. |

Estimated 2024+ | The UK has lost c.15% of its intertidal habitat since 1945 and has approximately 45,000ha of saltmarsh habitat remaining.

It is assumed that saltmarsh carbon credits will be priced higher than peatland or woodland carbon credits due to the high restoration costs as well as the potential carbon emissions generated during the restoration process itself, though maintenance and monitoring costs are expected to be minimal. Given the nascent stage of the saltmarsh carbon market and the lack of comprehensive data on carbon sequestration rates, it is expected that impact and mission-aligned investors are more likely to be interested in investing in these projects. This project is being supported by the Natural Environment Investment Readiness Fund, which gave funding to the project in its first round in 2021.

|

| Woodland Water Code | The Forestry Commission is exploring development of a Woodland Water Code to provide a standard for water-related benefits of woodland creation such as pollution mitigation, flood risk mitigation and river flow support, and enable markets for these. |

Estimated 2025+ | Announced in the UK Nature Markets Framework, published March 2023

Methodology is to comply with the UK Woodland Carbon Code. |

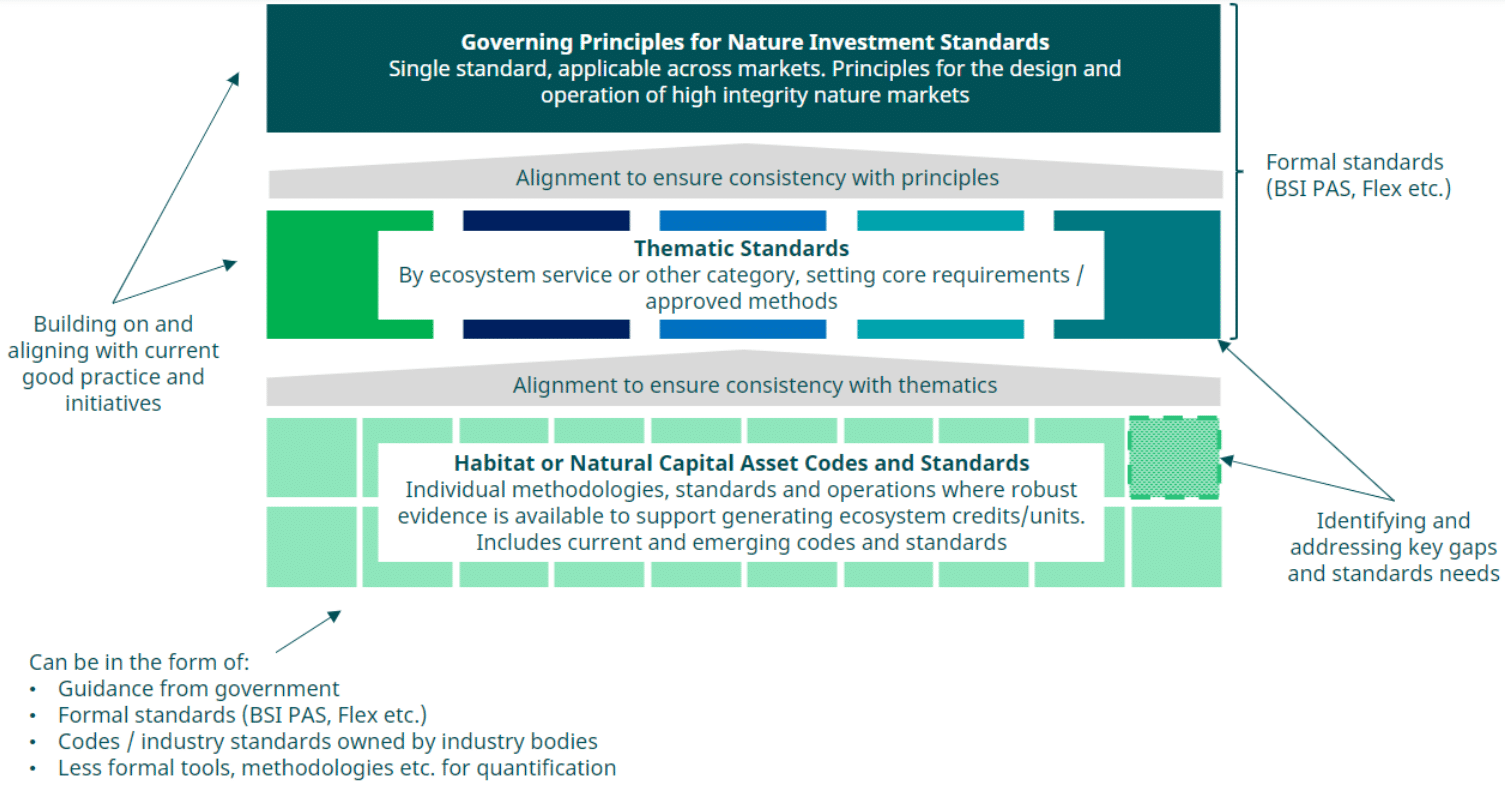

To support the scaling of high-integrity environmental markets, Defra has announced a three-year partnership with the British Standards Institute to develop a UK Nature Investment Standards Programme. This will include a new, consensus-based, UK-wide standards’ framework, which sets out clear principles and requirements. This builds on previous recommendations from the Financing Nature Recovery Coalition that the UK government establish a system of standards for quantifying environmental services from nature, including an assessment process for individual standards.

BSI will work across all devolved Governments, to facilitate an industry-led process. This will develop a suite of interconnected investment standards across ecosystems services. These UK wide standards will drive the application of consistent principles and approaches to the quantification of ecosystem services. They will provide a benchmark by which successful methodologies can be recognised as sufficiently robust and credible.

Nature Markets Framework, Defra, 2023

Defra is scoping out the most appropriate role for government in overseeing markets, in particular what its role should be in ensuring that data on credit transactions is systematically and publicly available.

You can read more about this work on the BSI’s Nature Investment Standards Programme website, including a useful summary flyer, and a short survey to give your views.

The BSI also hosted a launch webinar on the 18th of May, where BSI shared their emerging framework, linking this to the Government’s Nature Markets’ Framework, (with opening words from Lord Benyon), and gathering views from the National Farmers’ Union the Green Finance Institute and RSBP who gave the perspectives of land managers, buyers and other market participants. If you missed this, you can download a recording of the webinar here: Nature Investment Standards programme webinar | BSI (bsigroup.com)

Stacking and Bundling

‘Stacking’ and ‘bundling’ are mechanisms for packaging and selling environmental services from nature. The terms describe whether and how different environmental services can be sold separately from the same piece of land, or sold as a single product reflecting more than one

service.

In the Nature Markets Framework, published March 2023 by Defra, the following definitions are set out:

Bundling: When a suite of ecosystem services produced by the same activity (for example the biodiversity and water quality improvement provided by wetland restoration) is sold as a single combined unit in the market.

Stacking: When multiple different ecosystem services produced by the same activities (for example biodiversity and carbon benefits of a new woodland) are sold as separate units in the market.

The government recognises that stacking is an important concept to support achieving multiple environmental outcomes and intend to give support for greater use of stacking as well as explicit bundling.

While ruling that stacking within compliance markets is permissible (see below), Defra will conduct a market and policy analysis to determine whether a greater degree of stacking should be permitted between compliance and voluntary markets. This will include consideration of environmental outcomes and implications for market dynamics across all markets.

The below rulings have been set out by the responsible bodies and summarised in the Nature Markets Framework.

Biodiversity net gain (BNG) and Nutrient Mitigation

Phase 1 guidance permits units to be issued for both BNG and nutrients from the same activity/project. They do not permit units to be issued for BNG or nutrients and also for a voluntary ecosystem market from the same activity/project, unless through a subsequent habitat improvement. This improvement needs to be quantified in comparison to a baseline which includes the initial activity.

UK Woodland Carbon Code

The WCC states that currently the wider benefits of woodland creation projects are ‘bundled’ with the carbon unit by default when they are sold. In future, the WCC Secretariat may agree additional ecosystem service standards that can be stacked with the WCC. Once agreed and the necessary registry infrastructure is in place to keep track of ‘stacked’ and ‘bundled’ projects, woodland creation projects should be able to stack these standards with WCC provided that all income streams are declared in the WCC Cashflow Spreadsheet and the project meets required additionality tests. The potential to credit water or biodiversity and stack with carbon

credits is being investigated.

UK Peatland Code

As with the UK Woodland Carbon Code, the Peatland Code’s guidance states clearly that units are currently sold as an implicit bundle in which other ecosystem services associated with peatland restoration (such as biodiversity and water-related benefits) are ‘bundled’ in with the measured carbon unit. The UK Peatland Code notes that in future it may be possible to stack multiple voluntary credits where these meet the additionality criteria of the Code, and again provided the right registry infrastructure is in place to prevent double counting, and is exploring how this could be done.

If you would like to learn more about the concept and practicalities of stacking and bundling, the GFI recommends the below resources:

- Natural Capital webinar: stacking and bundling, Mills and Reeve, Tellus Capital, 2023

In this session, Andrea Newman (Mills & Reeve) and Kate Russell (Tellus Natural Capital) reflect on the 2023 ELM update and the 6 added standards for the Sustainable Farming Incentive. Recorded on 2 March 2023 the webinar focuses on stacking and bundling.

- Stacking and Bundling Background Paper, Financing Nature Recovery Coalition, 2021

This short Background Paper has been prepared for participants in the Financing UK Nature Recovery: Stacking and Bundling Workshop that was held on the 22nd April 2021.

It includes a useful explanation on the difference between stacking and bundling, why this distinction is important in the context of environmental markets and nature recovery, and practical case studies of where these two concepts are applied.

- Theory and Practice of ‘Stacking’ and ‘Bundling’ Ecosystem Goods and Services: A Resource Paper, Business and Biodiversity Offsets Programme, 2018

This Resource Paper has been prepared for the Business and Biodiversity Offsets Programme (BBOP) by Forest Trends. BBOP ran from 2004-2018 to help developers, conservation groups, communities, governments and financial institutions develop and apply best practice towards achieving no net loss and preferably a net gain of biodiversity. Though this work’s scope is international, it contains useful insight as to the practical and policy-related challenges of stacking.

Government Strategies and Programmes of Support

Government support for nature restoration will continue to be a vital component in scaling the UK’s project pipeline. Nature restoration is an area considered separately by the Devolved Administrations. Each government has the right to develop its own strategy, corresponding targets, grant funding structures and market drivers to help meet these targets. Below are tables summarising, at a high level, each Government’s position on supporting nature-positive outcomes.

| Administration | Latest Strategy | Quantified Targets | Government Funding | Government – based Market Drivers |

| UK-Wide

|

Net Zero Strategy: Build Back Greener | Increase planting rates to 30,000 hectares per year by the end of the current Parliament and maintain this planting level at least from 2025 onwards. | – | UK Environmental Reporting Guidelines – accepts Woodland Carbon Units from the Woodland Carbon Code |

| Scotland

|

Climate Change Plan, 2018-2032

Scotland’s Forestry Strategy 2019 – 2029 Note: Includes Scotland Forestry Strategy Implementation Plan 2022-2025 |

Create 18,000 hectares of woodland annually by 2024

Create 4,000 hectares of native woodland each year by 2025 |

Nature Restoration Fund £65m | – |

| England

|

Environmental Improvement Plan 2023 | 12% land cover by 2060 – planting 180,000 hectares by the end of 2042

Treble tree planting in England by the end of the current Parliament. |

.Big Nature Impact Fund (BNIF) – £30m across different nature-based projects, funded by NCF.

Countryside Stewardship offers woodland-linked grants, including: Woodland Creation Planning Grant (England Woodland Creation Offer) |

Woodland Carbon Guarantee – £50m |

| Wales

|

Written Ministerial Statement | Plant 43,000 hectares of new woodland by 2030 and 180,000 hectares by 2050 – equivalent to planting at least 5,000 hectares per year.

Increase Woodland cover by at least 2000 hectares per annum from 2020 to 2030. |

Woodland Creation Grant

Small Grants – Woodland Creation Scheme |

– |

| Northern Ireland

|

“Forests for our Future” 2020 | Aims to plant 18 million trees or 9,000 hectares of new woodland over the next 10 years | Small Woodland Grant Scheme | – |

.

Icons created by Alexander Skowalsky from Noun Project

| Administration | Latest Strategy | Quantified Targets | Government Funding | Market Drivers |

| UK-Wide

|

Net Zero Strategy: Build Back Greener | 2,000,000 hectares of peatland in good condition, under restoration or being sustainably managed by 2040 (UK Peatland Strategy) | – | UK Environmental Reporting Guidelines – accepts Peatland Carbon Units from the IUCN UK Peatland Code |

| Scotland

|

Climate Change Plan, 2018-2032 | At least 280,000 hectares by 2030, including 20,000 hectares per year. | Peatland Action Fund – £250m | – |

| England

|

Environmental Improvement Plan 2023

Note: Plan Proposes the England Peat Implementation Plan (covering a more detailed trajectory to 2050, to be launched from 2024) |

At least 35,000 hectares by 2025.

Approximately 280,000 hectares by 2050 |

Nature for Climate Peat Grant Scheme – £80m

Big Nature Impact Fund £30m – across different nature-based projects Countryside Stewardship (Environmental Land Management Scheme) – an enhanced version to replace plans for a Local Nature Recovery Scheme. |

– |

| Wales

|

National Peatland Action Programme (NPAP), 2020-2025 | Restore 1,800 hectares a year until 2025. | NPAP grants | – |

| Northern Ireland

|

Northern Ireland Peatland Strategy, 2022-2040 | 150,000 hectares under restoration or sustainable management by 2050 | Not yet announced

Note: DAERA is looking atways to develop a bespoke, long term funding mechanism which will build on current DAERA funding, including the Environment Fund |

– |

Icons created by Alexander Skowalsky from Noun Project

| Administration | Latest Strategy | Quantified Targets | Government Funding | Market Drivers |

| UK-Wide

|

Nature Positive 2030 | Protect at least 30% of land and sea cover for nature by 2030. | – | – |

| Scotland

|

Scottish Biodiversity Strategy to 2045 | Several ‘Priority Actions for 2030’, including:

|

Scottish Nature Restoration Fund (NRF) – £65m

Scottish Marine Environmental Enhancement Fund (SMEEF) – £3m |

Not yet announced

Note: The Scottish Government is currently discussing the use of biodiversity credits to mitigate biodiversity loss in Scotland, including through the use of compliance markets. Click here to watch a webinar ran by the Scottish Nature Finance Pioneers on this work. |

| England

|

Environmental Improvement Plan 2023

Forestry England Biodiversity Plan 2022-26 Note: Local Nature Recovery Strategies will be prepared across England from April 2023.

|

Restore 75% of 1m hectares of terrestrial and freshwater protected sites to favourable condition

Create or restore 500,000 hectares of wildlife-rich habitat outside of the protected site network |

Big Nature Impact Fund – £30m across different nature-based projects

Landscape Recovery (Environmental Land Management Scheme) – February 2023 update available here. Countryside Stewardship (Environmental Land Management Scheme) – launching in Autumn 2023. |

Biodiversity Net Gain requirement – applies to most developments under the TCPA from November 2023 and will apply to Nationally Significant Infrastructure projects (NSIPs) from November 2025, creating a compliance market. |

| Wales

|

Vital Nature | Designate 30% of land and sea cover as protected area by 2030.

Note: The Welsh Government published its Biodiversity Deep Dive in October 2022 to explore practical actions for meeting this target. |

Nature Networks Fund (Heritage Fund) | Biodiversity Net Gain requirement – applies to most developments under the TCPA from November 2023 and will apply to Nationally Significant Infrastructure projects (NSIPs) from November 2025. |

| Northern Ireland

|

– | – | Environmental Farming Scheme | – |

Icons created by Alexander Skowalsky from Noun Project

| Administration | Latest Strategy | Quantified Targets | Government Funding | Market Drivers |

| UK-Wide

|

Water Framework Directive | Achieve ‘Good’ Ecological Status for 75% of water bodies by 2027. | – | – |

| Scotland

|

River Basin Management Plans (RMBPs) | – | Agri-Environment Climate Scheme (AECS) | |

| England

|

Environmental Improvement Plan 2023

River Basin Management Plans (RMBPs)

|

Improve at least three quarters of waterbodies to be close to their natural state as soon as is practicable | Big Nature Impact Fund – £30m across different nature-based projects

Landscape Recovery (Environmental Land Management Scheme). February 2023 update available here. Countryside Stewardship (Environmental Land Management Scheme) – an enhanced version to replace plans for a Local Nature Recovery Scheme. |

Nutrient Neutrality requirement – applied across 74 Local Authorities to property developers

Note: A National Nutrient Mitigation Scheme, managed by Natural England, is expected to be launched in 2023. Water industry national environment programme (WINEP) – applied to water companies |

| Wales

|

River Basin Management Plans (RMBPs) | – | Nutrient Management Investment Scheme | Nutrient Neutrality requirement – applied to certain property developers, affecting catchment areas across 15 councils and National Park Authorities. |

| Northern Ireland

|

River Basin Management Plans (RMBPs) | – | Environment Fund – Water Quality Strand | – |

Icons created by Alexander Skowalsky from Noun Project

| Administration | Latest Strategy | Quantified Targets | Government Funding | Market Drivers |

| UK-Wide

|

– | – | – | – |

| Scotland

|

Flood Risk Management Strategies (FRMS) | Some NFM measures can be funded through Local Authority budgets, where they support their Local FRMS. | ||

| England

|

Environmental Improvement Plan 2023

Flood and coastal erosion risk management policy statement National Flood and Coastal Erosion Risk Management Strategy for England Flood Risk Management Plans (FRMPs) Note: 2021 – 2027 FRMPs are due to be published in 2023

|

Double the number of government funded projects which include nature-based solutions to reduce flood and coastal erosion risk. | Flood Defence Grant in Aid (GIA) – for Risk Management Authorities only

Community Infrastructure Levy – granted by Local Authorities Local Levy – made by Regional Flood and Coastal Committee Landscape Recovery (Environmental Land Management Scheme). February 2023 update available here. Countryside Stewardship (Environmental Land Management Scheme) – an enhanced version to replace plans for a Local Nature Recovery Scheme. |

Partnership Funding Approach |

| Wales

|

The National Strategy for Flood and Coastal Erosion

Risk Management in Wales, 2020 Flood Risk Management Plans (FRMPs) Note: 2022 – 2028 FRMPs are due to be published in 2023. |

– | – | – |

| Northern Ireland

|

Flood Risk Management Plan 2021-2027 | – | – | – |

Icons created by Alexander Skowalsky from Noun Project