Project Summary

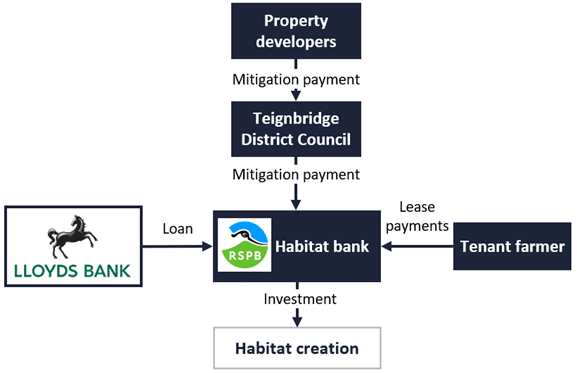

Ashill is a 37-hectare rural site located in Devon and was acquired by the RSPB to create a habitat bank. This was to help offset the impact of housing expansion in the area on the loss of the cirl bunting, which is a protected farmland bird species under threat. The land acquisition was refinanced with a from Lloyds Bank is being repaid over five years with designated Section 106 funding from Teignbridge District Council. It is one of the first examples of up-front private investment being supported by S106 payments towards a nature-based outcome. The project team was led by the RSPB and Finance Earth, which worked closely with the Teignbridge District Council.

Acknowledgements

With many thanks for their time and insight on this case study:

Paul Cottington, Head of Conservation Investment, RSPB

Jack Rhodes, Environmental Consultant, RSPB

![]()

Rich Fitton, Senior Associate Director, Finance Earth

![]()

Date published: 05/03/2023

Financial Innovation

The key financial innovation of this project has been the use of repayable finance to support a new habitat in advance of harm caused by developments, rather than afterwards. This was achieved by using an anticipated but uncertain future income stream within one local planning authority, creating a contracting mechanism to secure those future payments for mitigation activities through Section 106 (“S106”) payments, and subsequently raising a £0.5m term loan secured by this contract.

This has allowed the RSPB to move away from the traditional ‘donative income’ model for nature restoration that relies solely on RSPB cash balances, allowing for a more efficient financial structure. Ashill was previously acquired by the RSPB in 2017 through its cash balance, so the term loan in this project effectively refinanced this purchase in 2020 and the RSPB was able to deploy their capital elsewhere, including other conservation programmes.

This structure is also beneficial to local councils. While S106 payments are intended to compensate certain impacts of development, local councils responsible for the deployment of funds for compensation measures typically struggle to spend the incoming funds, with significant amounts remaining unallocated within the planning system.

Finance Earth and the RSPB designed a financing mechanism to provide an “off-the-shelf” solution for the local council and housing developers in the form of a habitat bank, enabling the efficient allocation of compensatory payments into a suitable mitigation scheme (the habitat site) that was already established. This has removed the time gap between the damage caused to the environment by the developer and the establishment of compensatory habitat, thus removing the council’s risk of failing to ensure no net loss of the cirl bunting habitat.

Project Structure, Finance Earth Presentation, 2022

Building the financial model

The financial model of this project is structured as a cashflow projection on Excel over a five-year period. It was developed by Finance Earth, which undertook the financial modelling and analysis of projected cashflows, in collaboration with the RSPB and the local council.

Capturing Income

-

- Mitigation payments from local developers

The main revenue stream of the project is built on expected ‘mitigation payments’ made by property developers for the harm caused by their developments to the cirl bunting, a now rare bird species in the UK rarely found outside of South Devon.

As the cirl bunting is a priority species under the NERC Act 2006, housing developers must mitigate any impact from development on the cirl bunting’s habitat. Compensation payments are acceptable as the third and final stage of the ‘mitigation hierarchy’ for developers (after “avoid” and “mitigate” onsite), but must be spent on suitable compensatory habitat in a suitable location and at the appropriate scale. The pricing for these mitigation payments varies per breeding territory and is set by the relevant local authority.

Such payments form the primary revenue stream of this financial model. The local planning authority Teignbridge District Council (‘the council’) had previously calculated that 2.5 hectares of compensatory habitat is required for each pair lost to any development. These mitigation payments are approved and administered by the council through the planning system via contracts known as Section 106 Agreements between the developer and the council.

The RSPB worked with the council to agree an appropriate total payment for the 37-hectare site, which it had identified near to proposed developments and a breeding territory of cirl bunting. This total income amount is fixed and to be given over five years from the council to the RSPB. It was set at a level to cover land purchase costs and the RSPB’s management and monitoring costs for the first five years. £200k in mitigation payments was immediately available for the site from the RSPB’s own sources, but a further c.£700k would be needed over five years to cover loan repayments.

There was a high degree of uncertainty about the timing of mitigation payments from the local council, as it is dependent on the demand from developers. This was identified as one of the major risks of the project, which is carried by the RSPB, as it has taken a commercial term loan onto its balance sheet that may take more than five years to repay, if receipts from mitigation payments are not sufficient.

To mitigate this uncertainty, Finance Earth, RSPB and the Local Authority reviewed planning commitments between developers and the council. This analysis included a forecast of planning applications and the actual proposed impact of each development on local cirl buntings, which was all provided by the council. Additional consideration was needed on the timing of payments due to the fact that, typically, S106 payments are not required until the underlying housing unit(s) is sold. As a result, there was certain confidence in the level of projected demand, but lower confidence in the timing of such demand and ultimately payments.

To mitigate this uncertainty, the project team took a more conservative approach to the estimates by building in an income buffer (minimum cash balance) into the financial model, along with expected delays to the receipts of mitigation payments and discounts on payment values. Finance Earth also tested these income assumptions in its sensitivity analysis (see below).

Overall, it was estimated that enough mitigation payments would be made within a five-year period for the RSPB to meet this obligation. As this was conducted on the balance sheet of the RSPB and all income was used for charitable purposes, this operational income is exempt from VAT and income tax.

The income stream was secured by a grant agreement between the RSPB and the Teignbridge District Council, which stipulates certain performance metrics relating to the cirl bunting population. It was agreed that the habitat bank operator (RSPB) would safeguarded the 52 pairs of cirl bunting living within 2km of the site, increase the number of breeding pairs within a defined period.

-

- Lease payments from the farmer

The second source of income for this project is rental payments from farmers managing the land, according to leases signed with the RSPB.

As cirl bunting populations can flourish alongside agricultural production, the project team decided to create an additional revenue stream by leasing the site back to the farmer (vendor) from whom it had initially acquired the site, under a Farm Business Tenancy. This lease then stipulates farming practices that support the cirl bunting population, such as the use of tussocky pastures, scrubs, large hedges, spring barley planting and winter stubble.

Requirements of this lease needed to meet both these views of the RSPB on supportive farming practices, and also the conditions for ‘compensatory habitat’ in accordance with the National Planning Policy Framework. This meant additional consideration was needed around the structuring of the lease agreements’ conditions. The project team engaged with Hewitsons LLP for forming this lease agreement and its wider legal work.

The ability to farm the land in a nature-friendly way has allowed a long term farming income stream and also land values being left intact. For the first five years, these fixed lease payments will be used towards the interest payments for the term loan, while payments afterwards can contribute to ongoing monitoring and management costs. This second funding stream and its co-benefits strengthened the commercial appeal of the project to all stakeholders, including the RSPB, the local council and the lender (Lloyds Bank).

Capturing Costs

Over this five-year period, the financial model captures land acquisition costs, the management and maintenance costs undertaken by the RSPB, and the financial costs (interest payments) of the term loan. The land acquisition made up the majority of total project costs at c.£850,000.

Other costs not captured in the model include the management and monitoring costs after the five year period, RSPB’s legal costs, and the project development costs – mainly consisting of RSPB employee time but also the fees paid to Finance Earth as advisor. RSPB agreed to pay for these, partly through its core funding, but management and monitoring costs after five years may also be supported by future lease payments from the farm tenants of the site.

As the cirl bunting population can be supported by minimal interventions, such as the use of spring barley, there were no habitat ‘creation’ costs to the project. The farmer has committed to making and maintaining these interventions with any technical support needed to be provided by the RSPB.

To capture the project costs, the RSPB had ample expertise and knowledge from its Land Agent teams. All major cost assumptions, such as the land value, were easier to estimate due to this in-house expertise and other relevant third parties such as the Local Planning Authority.

As the RSPB is a registered charity, there were minimal tax implications on the cost side, with its status exempting it from taxes such as Stamp Duty Land Tax on the site acquisition.

The project team comments that the five-year timeframe of the financial model gave the project team a stronger degree of confidence in these assumptions compared to longer timeframes associated with habitat bank models. Inflation estimates were also factored into the management and monitoring costs over this period.

Structuring Investment

The project team agreed that a short-term, debt based investment would be best for the project, due in part to the predicted income streams and the RSPB’s established relationship with Lloyds Bank that offered debt-based investment. Through the mitigation payments, the project could repay this debt in portions (amortisation).

The project team approached Lloyds Bank with an ask of £500,000 and a timeframe of 4-6 years for full repayment, subject to interest rates offered and other conditions of the loan.

Strengths highlighted during Lloyds Bank’s due diligence process included the financially innovative aspects of the project (see above), the additional revenue stream from the farmer lease payments that would cover interest repayments, and the fact that the RSPB is effectively underwriting this transaction by taking the loan on its own balance sheet. The environmental impact of the project was also emphasised.

During due diligence, the lender mainly asked questions to understand where core revenue was derived from (S106 payments) and the types of contractual arrangements involved. The project team worked with Lloyds Bank to iterate the financial model, experimenting with different loan terms, such as interest rates. This took around six months.

An unsecured term loan of £500k was agreed in 2020, with initially a floating interest rate and regular repayment fee. There was also a transaction fee that was captured in the financial model.

Finance Earth led the structuring of up-front investment. This included the investor engagement to determine appetite and key terms, management of the investor due diligence process, negotiation of loan agreement terms and conditions and oversight of the loan transaction through to close.

Testing the model

To ascertain the financial robustness of the model, Finance Earth mainly tested two main groups of assumptions:

- Financing costs: Finance Earth sensitised the financing assumptions in reviewing loan options, mainly to assess the implications of a fixed vs floating interest rate.

- Income: Finance Earth also sensitised the timing of payment of mitigation payments from developers, the major risk of the project. A discount was applied to the forecasts to account for uncertainty.

The testing of these two aspects allowed Finance Earth and the wider project team to negotiate terms of the loan that minimised the risk of the project becoming overburdened with financial costs.

Conclusion

Through the innovative use of finance, the RSPB was able to shift from what to date has been an ‘in lieu’ scheme, whereby payment is used to deliver compensation post-damage; to a habitat banking approach, in which habitat is provided in advance of losses caused by development. Technically, this approach can be applied wherever the mitigation hierarchy is a requirement of planning, and there is an agreed methodology for calculating the level of compensation needed, whatever the level of that compensation (no net loss, net gain etc.).

The RSPB and its partners are measuring other ecosystem services across their landholdings now, such as the carbon flux of peatlands, to further explore project structures that capture the value of these ecosystem services. The project team comments that robust and reliable conservation science is key to unlocking these opportunities, such as this project, which was underpinned by extensive data and research on the cirl bunting and its value.

Sources:

- Interview with Rich Fitton, Finance Earth, 2023

- IRF Session 2: Becoming Investment Ready: Success Stories, Green Finance Institute, 2021

- A Guide to Cirl Bunting, RSPB

Photo credit: Ben Andrew (rspb-images.com)