Project Summary

The Cornwall AONB Partnership aims to channel private finance into nature across Section 08 of the Cornwall Area of Outstanding Natural Beauty (AONB), which is one of 12 sections of the AONB that cover 958 square kilometres. In 2020, the project team – Gain Consulting, University of Exeter and FWAG Southwest – found that a net environmental gain of up to £15.8m could be generated through its Landscape Recovery Framework, developed in partnership with 11 farmers in the AONB and other key stakeholders.

Throughout 2022, the project continued with grant funding from the Natural Environment Investment Readiness Fund (NEIRF). The project team has explored the feasibility of private investment into the farming sector and how to build the ‘supply-side’ of the project’s model. You can find full detail of the NEIRF project on its website, published by Cornwall AONB.

Acknowledgments

With many thanks to the following individuals for their time and insight:

Melodie Manners, Business Development Officer, Cornwall Area of Outstanding Natural Beauty

Collette Beckham, Director, Gain Consulting

![]()

Dr Grace Twiston-Davies, Research Fellow, Environment and Sustainability Institute, University of Exeter

Chris Knight, Director and Co-Founder, Terranomics

Tom Chellew, Senior Associate, Terranomics

![]()

Date Published: 15/02/2023

Identifying the seller base

This project is initially focusing on Section 08 of the Cornwall AONB, with plans to expand to the other 11 sections once they have an established model to scale. Cornwall AONB covers 958 square kilometres, of which 75% of land cover is farmed.

Section 08 of Cornwall AONB is the second-largest section of the Cornwall AONB, comprising 192 square kilometres (19,300 hectares), of which . Nearly three-quarters of the farms in Section 08 are owned directly by the farmer, with just over a quarter being tenanted, perhaps reflecting the high number of family, multi-generational farms. Most of these farms are of smaller size, between 50 – 150 hectares, and only 20% of farm holdings are more than 100 hectares.

The reasons for Section 08 being chosen for this project are set out in more detail in the Initial Project Scoping case study.

Approaching sellers and structuring engagement

As part of the Initial Project Scoping phase – driven by the Farming for the Nation Lizard Test Trial – the project team drew together a ‘cluster group’ of 11 farmers. The project team were already familiar with many farmers in Section 08, having worked with some of them in previous initiatives like ELM Advocacy.

When NEIRF funding was granted in September 2021 for the project’s further development, eight farmers agreed to continue this work and explore how private finance could be leveraged to meet the goals of the Landscape Recovery Framework that they had helped to build. The remaining three farmers declined due to other time commitments. The total land area within the farmer group is 1188 hectares with the average size of land under farmer management being 170 hectares.

Engagement was structured through a series of five workshops, hosted virtually, over the course of 2022. Each of these were followed by ad hoc surveys, phone calls, and farm site visits.

This work was mainly undertaken by three organisations in the project team; the University of Exeter, led by Dr Grace-Twiston Davies; Gain Consulting, led by Colette Beckham; and Terranomics Ltd, led by Chris Knight and Tom Chellew.

The project team comments that it was vital to work with the farmer group in a collaborative manner and not dictate what interventions should be placed on the farmers’ landholdings. It was also important to not underestimate the time needed to build trust with these groups on the topic of private finance, and the value of working with trusted partners with whom the farmers were already familiar.

Dr Grace Twiston-Davies of the University of Exeter gives a brief overview of working with the farmers throughout the Cornwall AONB project below:

Scoping farmer preferences for land use change

The first workshop with farmers was held in February 2022, giving an overview of what agri-environmental schemes would be available to the farmer group and the possibility of blending public and private income options. The project team also presented back the results of a survey they had asked the farmer group to complete, exploring potential land use changes.

This work differed from the overall Landscape Recovery Framework, developed in Initial Project Scoping, which set quantified targets for the whole of Section 08. The Landscape Recovery Framework was used to form the basis of the survey with the farmer group to identify the preferred opportunities for private finance and the amount of land possible.

The questionnaire showed that farmers saw the most significant opportunity in the diversification of pastureland, such as herbal leys or increasing the species richness of permanent pasture. They indicated that they could dedicate up to 49% of their land to this, and a further 27% of land cover to measures within rotational ‘mob’ grazing (27%). There was also significant interest in the restoration and planting of hedgerows, which many farmers saw as a tertiary ‘in field’ opportunity to sit alongside other interventions.

Increasing the extent of woodland was not seen as a significant opportunity at this time, as farmers generally perceived woodland planting projects as solely focused on carbon, and felt hesitant about selling carbon units to buyers that may use these to increase their carbon emissions elsewhere.

Exploration of payment mechanisms

Following on from this survey, the project team saw a mismatch between what farmers stated as the main opportunities to improve ecosystem services and current payment mechanisms.

In April 2022, another workshop was held to explore what Payment for Ecosystem Services (PES) mechanisms could help channel private finance to these interventions. An overview of current PES mechanisms was given at the start of the workshop.

The most popular mechanisms for Payments for Ecosystem Services were direct business investment (payment), grant funding and the Wilder Carbon Standards. The farmers viewed these as more flexible in allowing farmers to fit ecological improvements with their farming practices.

Wilder Carbon Standards was popular because it included actions to enhance biodiversity and wasn’t just focused on tree planting. The farmers viewed the sale of carbon credits via the Wilder Carbon Standards as a form of bundling, of which they generally approved.

Direct quotes from the farmer group on this topic include:

“I don’t like the idea that carbon’s being singled out. So, I quite like the bundling, because at least there are all the other benefits to it”

“We’re trying to achieve a sort of three-way split, which will, help insects, wildlife, birds, butterflies etc and hopefully the spin-off will be biodiversity and carbon opportunities”

Colette Beckham, Director of Gain Consulting, gives a brief overview of exploring the feasibility of private finance and exploring the ‘supply side’ of the Cornwall AONB project below:

Farm Profiles

Following on from the farmer opportunities survey and identification of the key PES transaction types, the project team identified three main interventions on the farms that could benefit from private sector finance in the nearer term:

- Woodland creation (via the Woodland Carbon Code)

- Wood Pasture creation (yet unidentified mechanism)

- Woodland, heathland, or species-rich grassland creation (Biodiversity Compensation Site)

Colette Beckham of Gain Consulting Ltd and Dr Grace Twiston-Davies of the University of Exeter then focused on the development of spatial plans for these three main interventions, using QGIS mapping and several overlayed datasets, such as the University of Exeter’s Ecosystem Service Opportunity Map for Cornwall AONB and the Natural capital map based on Land Cover (2005) from the Environmental Records centre for Cornwall and the Isles of Scilly (ERCCIS).

The University of Exeter and Gain Consulting spatially mapped the key opportunity areas for each farm. A full day site visit was then carried out with each farmer. The project team says that the farm site visits were particularly effective in exploring the opportunities.

A third workshop was held in May 2022 to present the Farm Profiles and discuss the potential offer of supply with the farmers. An example Farm Profile can be found here.

Overall, the intervention area for the PES opportunities amongst the Farmer Group is now estimated at 213 hectares, out of the total 1188 hectares that the eight farmers hold. The largest opportunities lie with Biodiversity Net Gain (up to 70 hectares) and Woodland Carbon (up to 72 hectares). Based on extrapolating these findings to the wider Cornwall AONB, the potential land available for use is estimated at 21,604 hectares, driven by Biodiversity Net Gain (approx. 5,435 hectares) and Woodland Carbon (approx. 5,255 hectares).

Barriers to supply

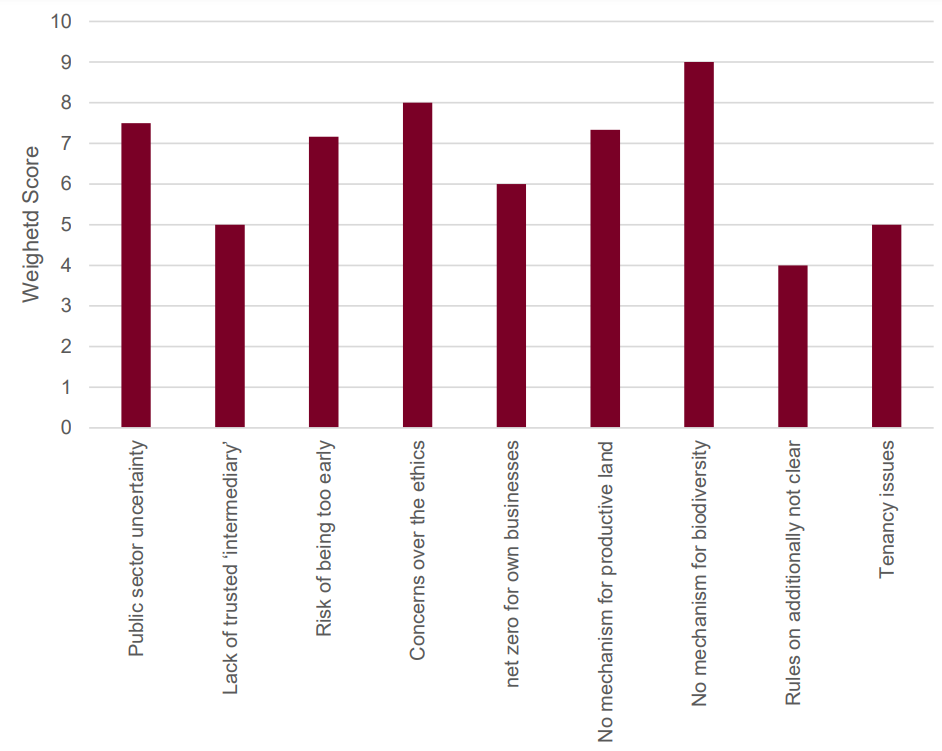

Following the creation of the Farm Profiles, the project team focused on the barriers that may prevent the farmers from deliver these interventions with private finance. A fourth workshop was held in August 2022 to discuss this, and the project team then compiled a list of key barriers. During the follow-up phone/Zoom calls, Twiston-Davies asked each farmer to rank these. The top-three ranked were:

- Public sector uncertainty / ELMs Local Nature Recovery scheme not yet ready

- No mechanism yet for farmers who want to ‘go the extra mile’ for biodiversity

- Concerns over the ethics and not being in control of who’s buying the credits

It was acknowledged during the workshops that PES opportunities are unlikely to be able to replace support from the Basic Payments Scheme and subsequent agri-environment schemes, given the current pricing on carbon credits and BNG units that the project team provided.

Given this need, the overriding barrier was uncertainty over the new ELM schemes. The farmer group desire a quicker roll-out of the ELM schemes and assurance over eligibility and payment levels, specifically within Nature Recovery. Linked to this was a lack of certainty on trading rules and additionality. Farmers wanted to be sure they did not disadvantage themselves by entering into legal agreements too early.

These barriers were closely followed by worries about engaging with private finance too early and the fact there is no mechanism available yet for using private finance on land that farmers want to keep food-productive – such as carbon credits from farmed soil and agroforestry. Farmers also regarded their role as food producers as fundamental.

Furthermore, the discussions indicated that unless there are clear ethical rules about who can participate on the demand side, or a mechanism for groups of farmers to have some control over who their credits go to, there will be little uptake on the supply side.

Direct quotes from the farmer group on this topic include:

“The limiting factor is we just don’t know the detail how will government payments be affected by private finance, we need more notice and more detail”

“You want your finger on the pulse, but you do not want to get distracted when something new comes along. What if there is a food crisis in 5 years’ time and it all changes? A farmer’s top priority is producing high-quality food”

“No matter how the transfer side of things is structured, the basis of that would be that you’re selling your carbon-positive effect to somebody else for them to carry out some carbon-negative effect”

Finally, the farmers also worried about the potential need to demonstrate ‘Net Zero’ status, such as to their customers and government, independent of any carbon credits sold. The farmers felt that there was a risk of selling the rights of their ecosystem services away and later being penalised for failing to ‘inset’ their own carbon or nature footprint.

Weighted score from answers to ‘Please rank the following key barriers to stopping you from entering into a private finance deal for carbon/ecosystem services /biodiversity in the short term?’, Appendix 10: Feasibility of private investment in Section 08, South Coast Western – Supply, University of Exeter, 2022

Incentives to supply

Alongside the discussion on barriers, the workshop included a discussion on what incentives could be offered, and similarly the project team asked the farmers to rank these.

The incentives were more or less a mirror of the barriers. The top-three ranked were

- Clear guidance from Defra on when they expect blended finance to start and on what level

- Clarity provided by Defra over new ELMs schemes

- Support to look for potential Biodiversity/carbon opportunities on the farm

However, the other highly ranked key incentives are more actionable in the short term, such as providing support for groups of farmers to measure and monitor carbon and look for biodiversity opportunities on the farm, which could help drive engagement on the supply side.

Chris Knight, Director and Tom Chellew, Senior Associate of Terranomics Ltd give a brief overview of the project team’s findings on barriers and incentives to supply:

Farmer learnings on private finance through the project

During the project’s phone/Zoom calls, Twiston-Davies asked the farmers how being involved in the NEIRF project had changed their views on private finance being used for nature restoration.

Overall being involved in the NEIRF project had a positive impact, specifically on awareness and knowledge of the different options for private finance. However, overall only a slight increase was recorded in farmer’s confidence around access to private finances in the short term, with slightly more increased confidence in the longer term.

It was clear that the process of being involved in the NEIRF project has been valuable in providing awareness and knowledge about private finance and opportunities on their farms.

Direct quotes from the farmer group on this topic include:

“It has been eye-opening the whole process, I’m glad I have been involved and something I’d recommend a farmer doing if they have the chance. I’ve looked forward to the meetings and always come away with a nugget of information”

“I’m keen to keep working with the AONB and experimenting with new opportunities. I’ll always keep looking for what’s next”

“I think we all started thinking – why would we want to make other people’s businesses look better than they are – but working with the group has shown this may not be such a problem and that ethics are being considered”

Along with writing up a full report of its findings for the NEIRF, the project team also recorded this direct feedback from one of the farmers it has worked with over the past year:

Next steps

Concluding the NEIRF project in September 2022, the project team have outlined a set of recommendations to take forward, based on what is in their scope of influence.

In the next one to two years, the team believes it is essential to; start building small pilot projects with farmers, including tenant farmers and their landowners; develop a farming sector communication strategy for Section 08 and the wider AONB; and create a clear set of ethics that determines what buyers are eligible for participating in the Cornwall AONB project.

In the next one to three years, the team also hope to explore potential deals using the Wilder Carbon Standards, involve more farming representation on the AONB board and offer more support for farmers to determine their own pathways to Net Zero.

Sources:

- Interview with project team, 2023

- Cornwall AONB NEIRF project website, including:

- Full NEIRF project report

- Appendix 2: Farm Opportunities Scoping Survey

- Appendix 3: Example Farm Profile

- Appendix 10: Feasibility of private investment in Section 08, South Coast Western – Supply

- Agri Environmental Schemes and Biodiversity Net Gain Guidance (February 2022)

- Brief Overview of Payment for Ecosystem Services (PES) Opportunities (April 2022)