Project Overview

A group of Wildlife Trusts and Finance Earth have created a financial model to deliver Biodiversity Net Gain (BNG) units with the use of upfront private investment, accelerating the delivery of high quality local habitat banks. The partnership includes four Wildlife Trusts – Berks Bucks and Oxon, Warwickshire, Cheshire and Surrey – that will create and restore habitats across their counties. By using private investment to create the habitats in advance of BNG sales, the Wildlife Trusts will have a higher volume of ‘post-enhancement’ units that will support the financial viability of the project over the long-term and remove the time delay between nature loss from development and off-site habitat creation.

Acknowledgements

With many thanks for their time and insight on this case study:

Prue Addison, Conservation Strategy Director, Berkshire, Buckinghamshire and Oxfordshire Wildlife Trust

![]()

Alicia Gibson, Senior Associate Director, Finance Earth

Allan Benhamou, Associate, Finance Earth

![]()

Date published: 26/06/2023

Building the financial model

The Wildlife Trusts (WTs) worked with Finance Earth to build an investment model for three pilot sites to enable a consistent approach to financial analysis. This allowed the project partners to develop assumptions and analyse financial characteristics across multiple pilot projects, comparing required activities, delivery costs, market pricing and BNG unit sales strategy. Prue Addison, Conservation Strategy Director of Berkshire, Buckinghamshire and Oxfordshire Wildlife Trust (BBOWT) says it was important to test the model with different pilots in order to demonstrate the replicability of the model and maximise learnings. You can read about the sites in Initial Project Scoping.

Determining Sales Strategy

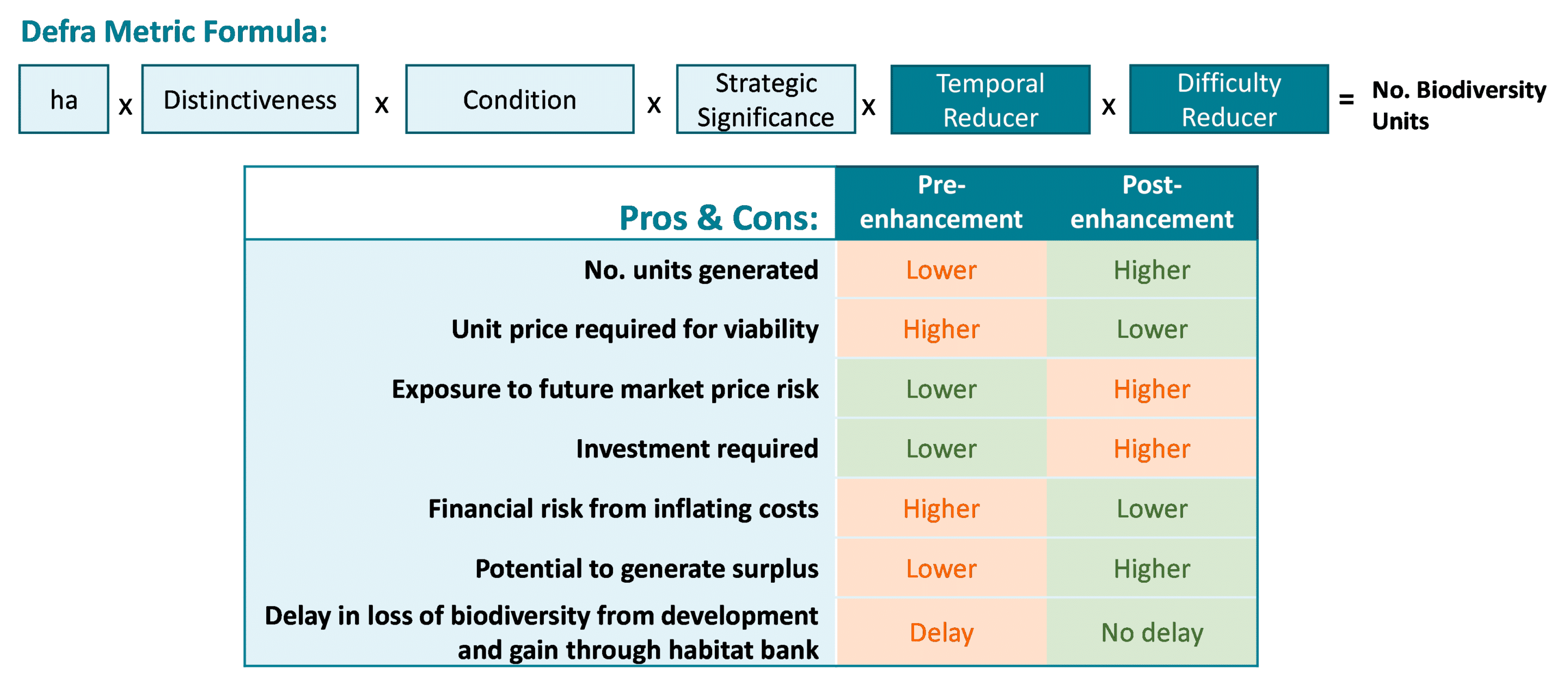

The investment model’s revenue is derived from the sale of biodiversity units, calculated through Defra’s BNG metric. Notably, the metric allows for ‘pre-’ and ‘post-’ enhancement sales, which factor in ‘temporal’ and ‘difficulty’ reducers affecting the number of units available for sale overtime. If BNG units are sold to developers before a habitat becomes fully established, this significantly reduces the number of units available for sale.

The project team identified several pros and cons of the differing sales strategies. For example, the ‘post-enhancement’ sales strategy may support site financial viability through a higher volume of units generated, and therefore a lower minimum unit price needed to meet lifetime costs. However, this would also require financing to meet up-front costs and expose the project to uncertain market demand in the future.

The project team concluded that a blended strategy – selling portions of both pre-and post-enhancement units – is likely to be the preferred approach.

Diagram 1: Overview of BNG sale strategies

While a blended sales strategy can be used for BNG sites – selling portions of both pre-and post-enhancement units – the project team needed to determine the appropriate balance for each site.

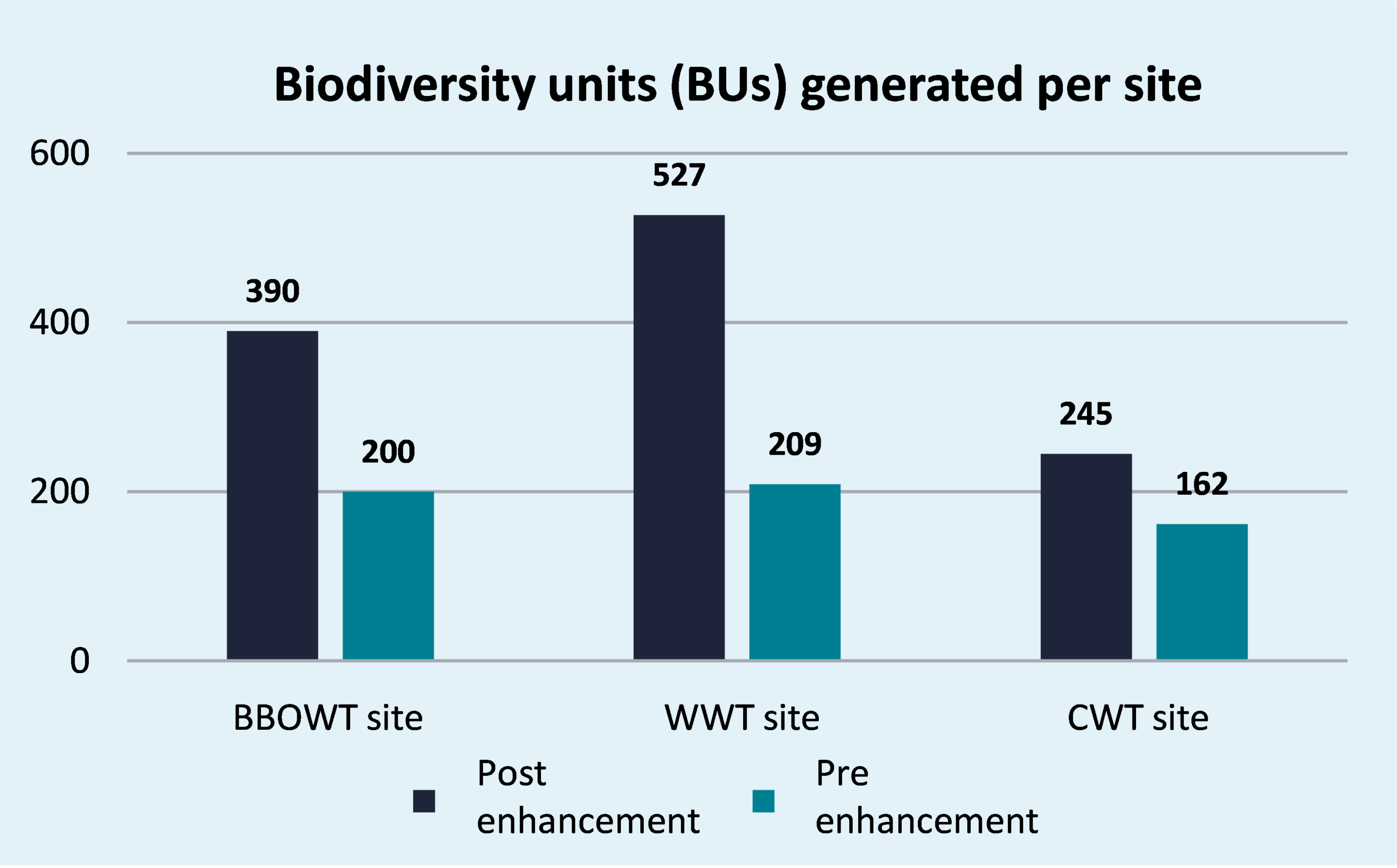

It calculated that all three pilot sites could deliver 540 units with a full pre-enhancement sales strategy and 1,132 units with a full post-enhancement strategy – termed a “habitat banking sale approach”. Assuming a fixed price of £20,000 per unit over time (eftec BNG market analysis, 2021), these strategies could generate between £11m-22m of undiscounted BNG revenues over 30 years.

Figure 1: Application of the Defra Metric to calculate BU generation across WT pilot sites

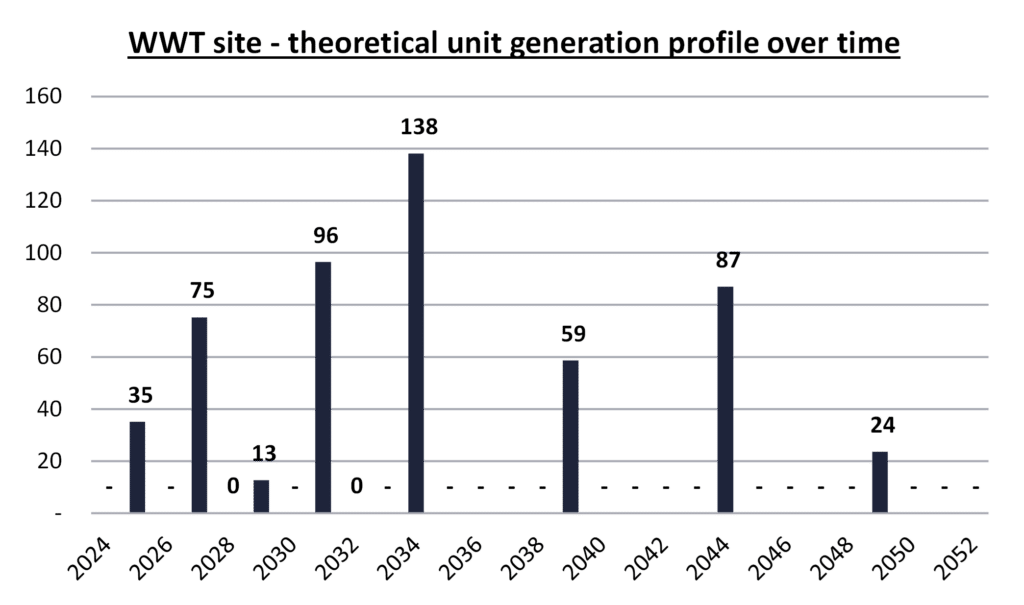

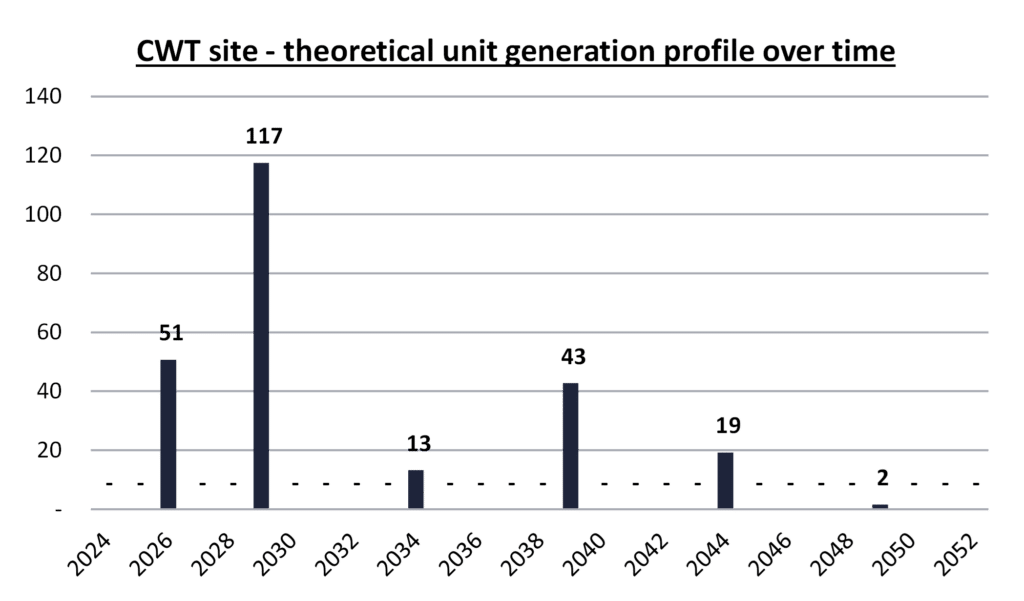

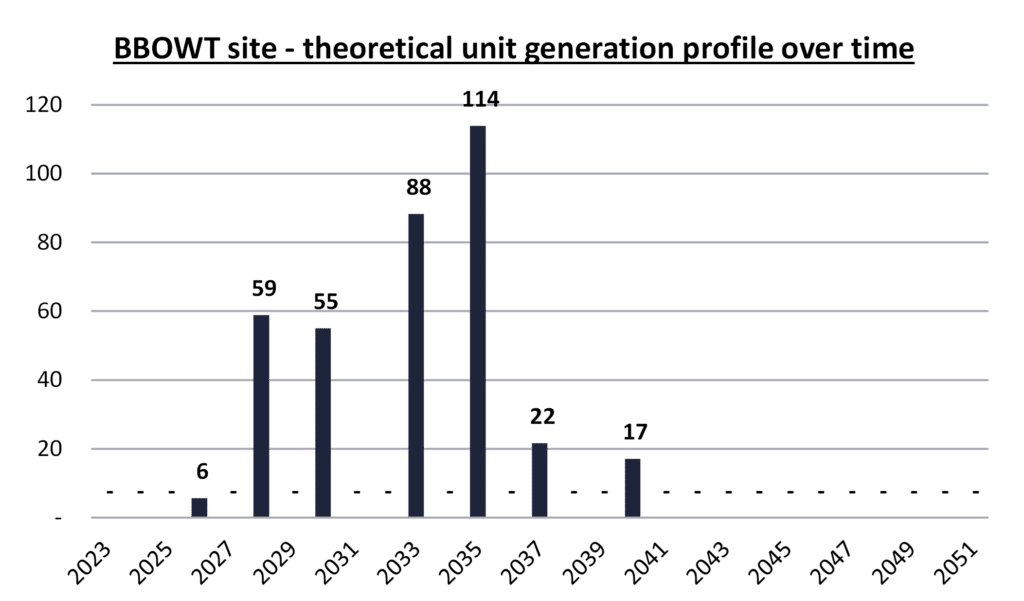

The graphs below show the indicative timeframe required to generate the full habitat banking sale approach (1,132 units) based on the metric’s assumptions, using a ‘step sale’ approach that allows units to be sold as the habitats reach different stages of quality.

Figure 2, 3 and 4: theoretical unit generation profile over time for each WT pilot sites, based on Defra metric timeframe

To determine the best strategy for each site, the project team assessed:

- Future development demand in the local area: higher confidence in the future demand from developers within the Local Planning Authority favours a post-enhancement sales strategy. As a precaution in modelling the project financials, the project team also decided to include a ‘buffer’ of units that would not be sold, to account for lower demand compared to units available.

- The ‘time’ and ‘difficulty’ reducers within the BNG metric. In some cases, the discount was so significant – up to 90% of potential BNG units – that the project was not viable if units were sold pre-enhancement. This was weighed against the strategic incentive of selling BNG units early on to build the WTs’ credibility and generate interest from buyers.

- Delivery costs: sites with lower delivery costs are more likely to be viable with an pre-enhancement sales strategy compared to those with higher delivery costs.

The sites are expected to generate most of their revenues in the first 10-15 years, based on the timeframe for habitats to reach maturity and the indicative sales strategy. Defra also confirmed that BNG sale receipts are subject to Value Added Tax (VAT).

Capturing Costs

To accurately capture costs, the WTs undertook a full comparison of their previous data on creating and maintaining habitats over several decades – including resources and time commitment for specific habitats, broken down per hectare. Along with input from ecological consultants such as Middlemarch Consulting, which had previously surveyed one of the sites, this allowed the WTs to estimate both the upfront management and maintenance costs, along with monitoring costs across the 30-year period with a high degree of confidence. Contingency costs were added across all costs, varying between 10-30% depending on WT preferences, to account for uncertainties over the project lifetime.

The WTs factored in monitoring costs based on both the expectations of requirements from the current BNG legislation, and monitoring of broader outcomes, such as species abundance and ecosystem services. A conservative monitoring estimate was included based on uncertain BNG monitoring requirements over the project period.

No additional governance or legal costs were included due to the plan for WTs to deliver projects through existing teams and organisational structures.

Inflation was set at 2.5% per annum. The project team also considered the use of an endowment structure to address inflation risk. A portion of the proceeds from BNG units sold could be allocated into an interest-bearing account or invested in low-risk gilts to hedge against inflation.

Sensitivity Analysis

Once a relatively complete picture of the model’s costs and revenue potential was captured, the project then tested several assumptions to determine the financial viability of the project.

The project team carried out sensitivity analysis for:

- BNG prices – both increases and decreases across the 30-year period

- Buffer rates – the percentages of units not sold to model potential insufficient demand across pilot site areas

- Varying sales strategies – selling more or fewer units upfront for each site

- Delays to habitat creation / restoration work of up to five years

- Increases in cost inflation rates

- Three to four different monitoring scenarios that varied extensiveness of monitoring plans

The main measure of financial viability was the net cash flow position, though in some cases where upfront investment was considered, the project team also calculated the Internal Rate of Return (IRR) and the net leveraged cash flow, which reflects the cash position after repayments to any investors.

Allan Benhamou, Associate at Finance Earth, says that the main elements that were tested were the BNG unit price and the buffer rate. He comments that the challenges of the investment modelling was “knowing where to draw the line, as you can pull so many different levers at this stage, but it is important to agree the reasonable assumptions around specific variables, and not get carried away with too many versions of the model.”

Lessons Learned

In the development of the investment model and business case, the project team noted several key lessons, including:

- The need for patience and adaptability: the approach required multiple iterations as challenges were identified and overcome, such as preferred sales strategies, approach to developing 30-year costings, expected type of investment, dealing with policy uncertainty etc.

- Collaborate and work with others: this project benefited hugely from working with four different WTs across the different pilot projects. Learnings were shared throughout the project, enabling progress to be made as a group if certain pilot projects or sales negotiations were able to advance quicker than others.

- Timeframes and resources required were above what is expected: a wide range of team members across the organisations need to be involved, the timeframe to develop an investable model is likely to be more than one year (the time given to the project from NEIRF funding – See Milestone 1). The model will continue to be iterated by the WTs.