Insurance and pensions fund investors can unlock capital to accelerate the green transition

Investment of £1trillion in UK infrastructure is required to reach net zero by 2050. The only solution for reaching this figure is private investment. Insurance and pension fund investors can play a key role in unlocking this capital if some simple solutions are put in place to overcome existing barriers.

The UK’s insurance and pension fund investment sectors have over £3 trillion assets under management and, given the potential cash flows and security offered by infrastructure assets, a desire to invest in sensibly structured solutions. Today, however, such investment is being held back by a lack of requisite performance data to satisfy private investors’ prudential investment mandates. Further, the private sector lacks the incentive to develop the financing solutions that would facilitate investment opportunities.

Both obstacles can be easily overcome. By blending well understood project finance techniques with targeted public support, the Green Finance institute has designed a number of sectoral solutions that it has tested with investors.

Working closely with the Investment Delivery Forum, established by the Association of British Insurers – and engaging with His Majesty’s Treasury, the Department for Energy Security and Net Zero, the UK Infrastructure Bank and the Office for Zero Emissions Vehicles – our primary focus has been to demonstrate the sector’s ability to invest £100 billion of capital in the green infrastructure transition over the next decade.

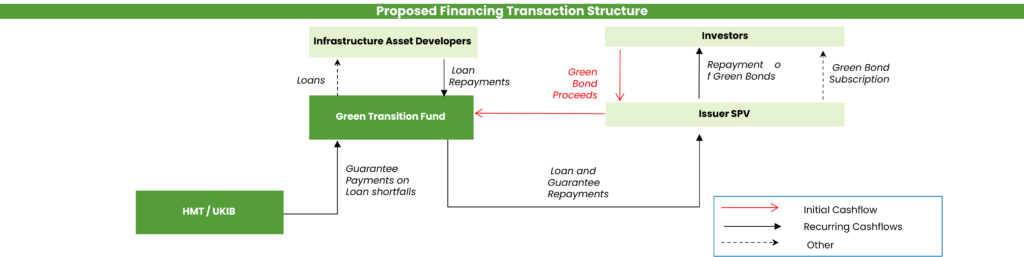

The solution ‘greenprint’

The solutions are built around the creation of sectoral Green Transition Funds which have been piloted by the GFI with investors . These GTFs crowd-in private finance where the public purse cannot stretch.

Using capital from insurance and pension fund investors through their subscription for bonds issued in the debt capital markets, the GTFs make loans to critical infrastructure developers. Repayments under these loans, which are secured on the relevant infrastructure assets, are the primary source of repayment on the bonds.

As the infrastructure assets lack the performance data to support investment in isolation, the government or other suitable body, such as the UK Infrastructure Bank, would ‘guarantee’ loan repayments at the launch of any GTF.

This guarantee can be structured as a simple guarantee, or by allocating a small portion of an existing environmental tax to cover any potential loan losses, such as a fraction of the around £25bn fuel duty raised by the government each year. There is indeed an inherent political and economic logic in leveraging existing environmental taxes to fund the green transition.

As the GTF programmes mature and performance data becomes reliable, public support would no longer be required – the government would have created mature, low cost, stable infrastructure funding programmes that introduce new sectoral ‘asset-classes’ with the right duration and risk profile to facilitate green infrastructure investment at significant scale from the insurance and pension fund sectors.

Benefits in Action

The application of this ‘greenprint’ to the EV public road charging network demonstrates the potential benefits of a GTF.

Today around 65 per cent of EV charge-point construction costs are funded through public grants, with little or no access to debt finance for most charge point operators. There are difficulties locating charge points in remote areas, and administrative frictions in planning/ licensing approaches persist. As a result, the infrastructure roll-out required across the UK is expensive to the taxpayer and well behind schedule.

A road charging GTF could replace grants with guaranteed loans, saving the public 65 per cent of up front construction costs. In addition, as the GTF would provide charge point operators with access to subsidised debt finance, this change of approach would promote competition and expedite the roll-out of charging points. It could also be used to address public policy objectives such as standardisation, expedited planning approvals and UK-wide coverage.

Assuming a construction cost of around £20 billion to deploy a national charging network, the GTF could save the taxpayer roughly £13 billion of sunk costs, while the running ‘cost’ to government would be represented by the amount drawn under the guarantee which is likely to be minimal.

A conservative loan loss rate of 5 per cent on £20 billion of funding under a GTF over 15 years would cost the taxpayer just £1bn – a leverage factor of private/ public funding of 20. Further, in reality, only a fraction of that amount would be needed to create a mature GTF platform that no longer requires government support.

In other words, the UK government could deliver a £20 billion nationwide charging infrastructure for a lot less than £1 billion over a 15 year period, while delivering steady returns to UK insurance and pension funds in a new asset class.

The road charging GTF is just one of the solutions that the GFI has piloted with ABI members through the IDF, and the ‘greenprint’ generally holds for other critical sectors.

The capital supply and demand are there for these solutions, and they are relatively simple to implement if we work together to deliver them. By facilitating investment, they can drive supply chains, significantly boost economic growth and reduce costs to consumers – paying for themselves environmentally and economically.